The single biggest financial decision you make when selling your home is not whether to use an agent. It is what number you put on the listing.

Price too high and your home sits on the market while buyers scroll past it. Price too low and you leave thousands of dollars on the table. In the 2026 Texas market, well-priced homes are selling in roughly 63 days. Overpriced homes are sitting for an average of 121 days, nearly twice as long. About one-third of all active listings nationally are sitting with a price cut (HousingWire, April 2026). Every one of those price cuts started as a pricing mistake on day one.

The tool that prevents that mistake is called a Comparative Market Analysis, or CMA. This article explains what a CMA is, how it works, why it matters more in Texas than in most other states, and how you can use one to set a list price that attracts offers without leaving money behind.

- What Is a Comparative Market Analysis?

- Why a CMA Matters More in Texas Than Most States

- What a CMA Includes

- How Comparable Properties Are Selected

- How Adjustments Work

- CMA vs. Appraisal: What Is the Difference?

- CMA vs. Zillow Zestimate

- Who Creates a CMA in Texas?

- How Waymark's AI Builds a CMA

- How to Read a CMA Report

- 5 Pricing Mistakes a CMA Helps You Avoid

- Frequently Asked Questions

What Is a Comparative Market Analysis?

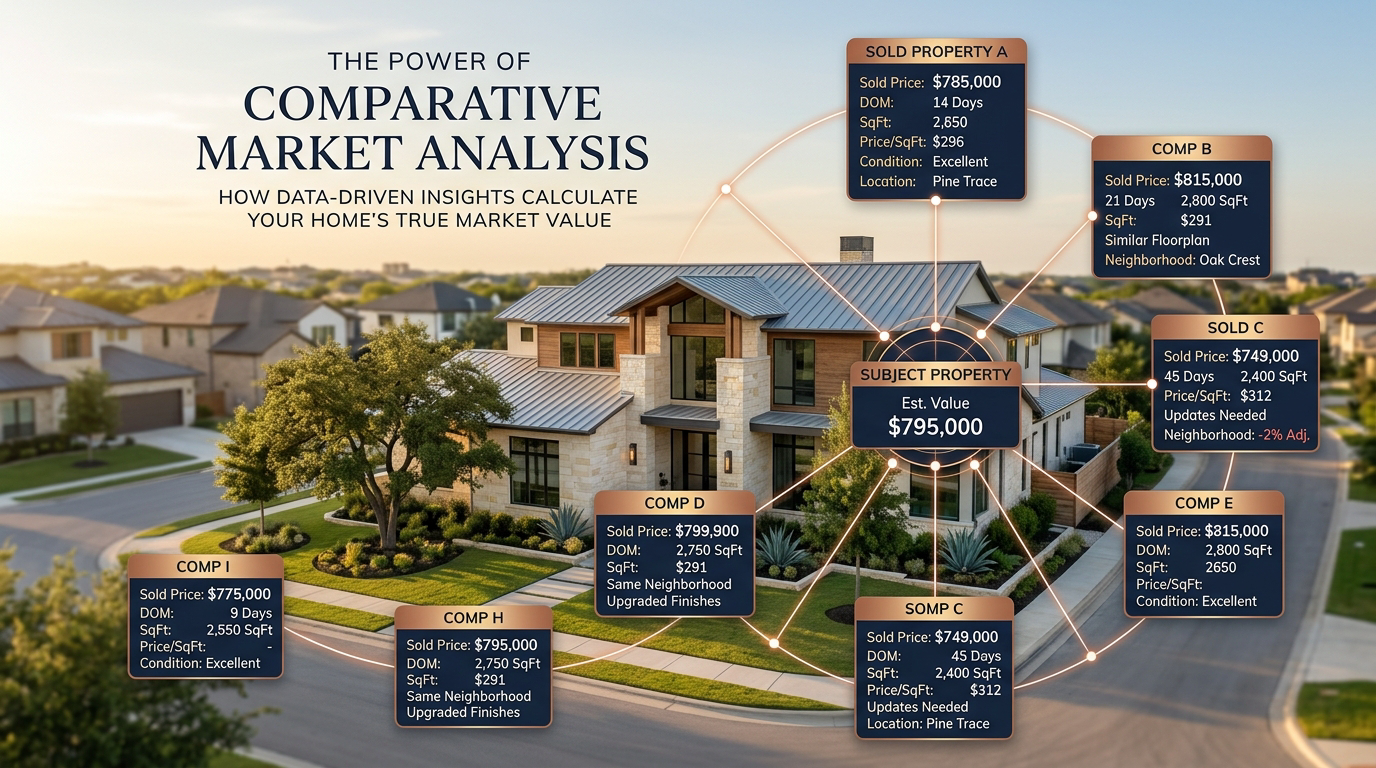

A Comparative Market Analysis is a report that estimates what your home is likely to sell for based on what similar homes in your area have recently sold for. It compares your property to recently sold homes (called "comps"), homes currently listed for sale, and homes that were listed but did not sell. The result is not a single number but a recommended price range based on real transaction data.

Real estate professionals have used CMAs for decades. The concept is straightforward: the best predictor of what a buyer will pay for your home is what buyers have recently paid for homes that look like yours, in the same area, in similar condition. A CMA takes that concept and structures it into a data-driven analysis that accounts for the differences between your home and the comps.

A CMA is not a guess. It is not what your neighbor thinks the house is worth. It is not what you paid for the home plus improvements. It is an analysis rooted in what the market has actually done in the last three to six months (Rocket Mortgage).

Why a CMA Matters More in Texas Than Most States

Texas is one of approximately 12 non-disclosure states in the United States. This means that when a home sells in Texas, the sale price is not recorded in public records. Unlike states such as California or Florida where anyone can look up what a neighbor's house sold for, Texas law does not require disclosure of real estate sale prices to any public body or database (SoldFast, 2026).

This has a direct impact on how sellers price their homes. Because sale prices are not public in Texas, websites like Zillow, Redfin, and Realtor.com cannot legally display actual sold prices for Texas properties the way they do in disclosure states. The "sold" prices you see on those sites for Texas homes are often estimates based on incomplete records, not the actual closing prices (Danny Buys Houses).

The actual sale prices are recorded in the MLS. Texas MLS rules require listing brokers to report sales prices promptly after closing. HAR's MLS rules, for example, require loading sales-closed information, including the selling price, within three days of closing (Texas Realtors). But MLS data is only accessible to licensed real estate professionals. The general public cannot access it.

This means a CMA built on actual MLS sold data is one of the only reliable ways to price your home accurately in Texas. Without it, you are pricing based on estimates, tax appraisal values (which often do not reflect market value), or guesswork. In a market where the gap between well-priced and overpriced homes means a 58-day difference in time on market, that guesswork is expensive.

What a CMA Includes

A thorough CMA report includes several categories of data that together paint a complete picture of where your home fits in the current market.

Subject property overview. This is your home. The CMA starts with the basic facts: address, square footage, lot size, number of bedrooms and bathrooms, year built, condition, and any notable features like a pool, updated kitchen, or recent roof replacement. These details determine which sold homes are fair comparisons.

Recently sold properties (closed comps). These are homes similar to yours that have sold in the last three to six months within your immediate area. For each comp, the CMA shows the original list price, final sale price, price per square foot, days on market, and any price reductions made before the sale. Closed comps are the most important data in a CMA because they represent what buyers actually paid, not what sellers hoped to get.

Active listings (current competition). These are homes currently for sale that are similar to yours. Active listings show you what you will be competing against. If three homes like yours are listed at $350,000 and you list at $400,000, buyers will notice the gap.

Pending sales. These are homes that have gone under contract but have not yet closed. Pending sales are a leading indicator of where the market is headed because they represent what buyers are agreeing to pay right now, not three months ago.

Expired and withdrawn listings. These are homes that were listed but did not sell. Expired listings are just as valuable as sold comps because they show you where the market drew the line. A home that was listed at $425,000 for six months and never sold tells you that $425,000 was above what buyers in that area were willing to pay.

Market conditions. A good CMA includes context about whether the local market favors buyers or sellers, average days on market, months of inventory, and any trends that could affect pricing. In the 2026 Texas market, conditions vary significantly by city and price point (Chase).

How Comparable Properties Are Selected

Not every recently sold home qualifies as a comp. The quality of a CMA depends entirely on how well the comparable properties actually compare to yours. Here are the factors that determine whether a sold home is a fair comparison.

Location. The closer the comp is to your home, the more relevant it is. Ideally, comps come from the same subdivision or neighborhood. Crossing a major road, highway, railroad, or school district boundary can change property values significantly, even if the homes are only a few blocks apart. In Houston, a house backed up against I-10 and a house on a cul-de-sac two streets away can have very different values despite nearly identical square footage (Absolute Properties HTX, 2026).

Size. Comparable homes should be within 10% to 20% of your home's square footage. A top Texas agent recommends staying within 500 square feet above and below the subject property, and tightening that range further if enough comps are available (HomeLight, 2026). Comparing a 1,400 square foot home to a 2,200 square foot home is not a meaningful comparison even if they are in the same neighborhood.

Age and condition. A home built in 2019 with a modern open floor plan is not a fair comp for a home built in 1985 with a traditional layout, even if they have the same bedroom count. The CMA should account for the overall condition of each comp, including any renovations, structural repairs, or deferred maintenance.

Features and amenities. A pool, a three-car garage, a primary suite renovation, or a new roof all affect value. The CMA should note which features each comp has that your home does not, and vice versa, so adjustments can be made.

Date of sale. The more recent the sale, the more relevant it is. In a shifting market, a home that sold eight months ago may have sold under very different conditions than a home that sold last month. Most CMAs focus on the last three to six months of sales data. In a volatile market, tightening that window to three months provides more accurate pricing (Luxury Presence, 2026).

The "rule of three." A reliable CMA uses at least three comparable sales. More is better, but three is the minimum needed to establish a meaningful range. Using fewer than three comps means any single outlier can distort the entire analysis (Chase).

How Adjustments Work

No two homes are identical. Even in the same subdivision, one home may have a pool while another does not. One may have a renovated kitchen while another has original finishes from 2005. Adjustments are how a CMA accounts for these differences.

The process works like this: if a comp sold for $380,000 and it has a pool that your home does not have, the CMA adjusts the comp's price downward to reflect what it would have sold for without the pool. If your home has a newer roof and the comp had an older roof, the CMA adjusts upward. These adjustments are applied to every comp for every meaningful difference.

Common adjustments include square footage differences (price per square foot applied to the difference), bedroom and bathroom count, garage size, pool, lot size, age of major systems (roof, HVAC, water heater), and overall condition.

After adjustments, each comp produces an "adjusted sale price" that reflects what it would have sold for if it had the same features as your home. The range of adjusted sale prices across all comps becomes the recommended price range for your listing. Most analysts recommend targeting the midpoint of that range in a balanced market, or slightly above in a strong seller's market (Rocket Mortgage).

CMA vs. Appraisal: What Is the Difference?

CMA Appraisal

Who creates it

Real estate agent, broker, or AI platform

Licensed appraiser

Purpose

Guide the list price for a seller

Determine value for a lender

When it happens

Before listing

After an offer is accepted, before closing

Cost

Usually free from agents, or included in listing service

$400 to $600 in Texas

Physical inspection

Not always (can be data-driven)

Yes, always in person

Legal standing

Opinion of value, not legally binding

Required by most lenders for mortgage approval

Data source

MLS, public records, agent knowledge

MLS, public records, physical inspection

A CMA helps you set the right price before you list. An appraisal tells the buyer's lender whether the agreed-upon price is supported by market data. They serve different purposes at different stages of the transaction. If your CMA is accurate, the appraisal should be close to the contract price. If the appraisal comes in lower, that creates an appraisal gap that must be negotiated between buyer and seller.

CMA vs. Zillow Zestimate: Why Online Estimates Fall Short in Texas

Many Texas sellers start their pricing research on Zillow, Redfin, or Realtor.com. These platforms provide automated home value estimates (Zillow calls theirs the "Zestimate") based on algorithms that analyze available public data.

The problem in Texas is that the most important data point, the actual sale price, is not public. Because Texas is a non-disclosure state, Zillow and other platforms cannot access the real sold prices that are locked inside the MLS. Their estimates rely on tax assessments, listing data, and mathematical models that try to infer what homes sold for without actually knowing the number.

This does not make online estimates useless. They can provide a rough starting point. But a CMA built on actual MLS sold data will almost always be more accurate in Texas than an automated estimate that does not have access to that data. For sellers who are basing their list price on a Zestimate alone, the risk is real: the estimate could be off by 5% to 15%, which on a $400,000 home is $20,000 to $60,000.

Who Creates a CMA in Texas?

Traditionally, a CMA is prepared by a real estate agent or broker who has MLS access. Most listing agents provide a CMA for free as part of their pitch to win the listing. Some agents who are not seeking a listing may charge $100 to $200 for a standalone CMA (HomeLight, 2026).

In Texas, the following professionals can create or access CMA data:

Licensed real estate agents and brokers. They have direct MLS access through boards like SABOR (San Antonio), HAR (Houston), ACTRIS/Unlock MLS (Austin), and NTREIS (Dallas-Fort Worth). They can pull actual sold prices, days on market, price-per-square-foot data, and listing history for any property in their MLS.

Licensed appraisers. They have access to MLS data and also conduct physical inspections. Their work product is an appraisal, not a CMA, but the underlying data is similar.

AI platforms with MLS data access. Newer platforms use comparable sales data to generate automated CMA reports. The accuracy depends on the quality of the data source and the sophistication of the analysis. A platform that uses actual MLS sold data will produce more accurate results than one that relies on public estimates.

How Waymark's AI Builds a Pricing Analysis

Waymark's AI, Aria, builds a pricing analysis using recently sold homes in your zip code. When you enter your property details (address, square footage, bedrooms, bathrooms, year built, features), Aria identifies comparable sales and presents them with sale price, price per square foot, days on market, and any price reductions.

What makes this different from a traditional CMA is that the seller has control over the comp set. If Aria includes a comp that is not a fair comparison to your home, maybe it is on a busy road, or it has a pool and yours does not, or it sold under distressed circumstances, you can remove it from the analysis. The recommended price range updates automatically based on the remaining comps.

On the Manage plan ($1,199), a licensed broker reviews the pricing analysis before the listing goes live. The broker can flag comps that may be misleading, suggest additional data points, or recommend a pricing strategy based on current market conditions in your specific MLS.

On the Launch plan ($699), the AI-generated pricing analysis is available without broker review. The seller sets the final price based on the data Aria provides.

Both plans include full MLS listing across SABOR, HAR, ACTRIS, and NTREIS with no percentage at closing. The pricing analysis is included in the listing fee. There is no separate charge for it. See Waymark pricing.

How to Read a CMA Report

When you receive a CMA, look at these elements in this order:

1. The adjusted price range. This is the most important number. It tells you the range within which your home is likely to sell based on what comparable homes have actually sold for. If the range is $360,000 to $385,000, your list price should be somewhere in that range.

2. Price per square foot. Compare this across all comps. If comps in your neighborhood are selling for $180 to $195 per square foot, and you are considering pricing at $210 per square foot, you need a strong reason (recent renovation, premium lot, view) to justify the premium.

3. Days on market. Look at how long each comp took to sell. If well-priced comps in your area are selling in 30 to 45 days, that is the timeline you should expect if your price is competitive. If comps that were originally priced higher took 90+ days and had multiple price reductions before selling, that tells you where the market drew the line.

4. List-to-sale price ratio. This shows the difference between what the seller originally asked and what the buyer actually paid. A ratio of 97% means the average home in your area sells for 3% below the original list price. This helps you decide whether to price at the top of the range (expecting negotiation) or at market value (expecting to attract more offers).

5. Expired listings. Do not skip these. Expired listings tell you what did not work. If a home with similar features was listed at $410,000 and never sold, pricing your similar home at $415,000 is a risk.

5 Pricing Mistakes a CMA Helps You Avoid

1. Pricing based on what you paid plus improvements. What you paid for the home and what you spent on renovations does not determine market value. A $30,000 kitchen renovation does not add $30,000 to the sale price. The market determines value, and a CMA shows you what the market is actually paying.

2. Pricing based on the Zestimate. Automated estimates in Texas are working without actual sale price data. They are a starting point, not a pricing strategy. A CMA built on MLS data is more reliable.

3. Pricing based on what you need. Needing $400,000 to pay off your mortgage and buy your next home does not mean your home is worth $400,000. A CMA separates what you need from what the market supports.

4. Pricing high "to leave room for negotiation." This strategy often backfires. Overpriced homes attract fewer showings, sit longer, and eventually sell for less than they would have if priced correctly from the start. In the 2026 market, one correct price beats three price cuts every time (NAR, 2025).

5. Ignoring expired listings. If similar homes did not sell at a certain price, that is data. A CMA includes expired listings precisely because they show you the ceiling the market rejected.

Frequently Asked Questions

How much does a CMA cost in Texas?

Most listing agents provide a CMA for free as part of their services. If you are not listing with an agent and want a standalone CMA, some agents charge $100 to $200 for the analysis. A formal appraisal, which is different from a CMA, costs $400 to $600 in Texas. Waymark includes a pricing analysis in both the Launch ($699) and Manage ($1,199) plans.

Can I do a CMA myself in Texas?

You can research comparable properties on your own using Zillow, Redfin, and county appraisal district records. However, because Texas is a non-disclosure state, the actual sold prices are not available through public records. Only licensed professionals with MLS access can pull the real closing prices. Without that data, a DIY CMA in Texas is working with incomplete information.

How often should I update my CMA?

Real estate markets can shift quickly. If your home has been on the market for more than 30 days without a serious offer, it is worth updating your CMA with the most recent sales data to see if the market has moved. Even a home that was well-priced at listing can become overpriced if the market softens during the listing period.

What is the difference between a CMA and an appraisal?

A CMA is an estimate of value prepared by a real estate agent or AI platform to guide pricing before listing. An appraisal is a formal evaluation conducted by a licensed appraiser, typically required by the buyer's lender before approving a mortgage. A CMA helps you set the price. An appraisal confirms (or challenges) that price after an offer is accepted.

Are sale prices really not public in Texas?

Correct. Texas is a non-disclosure state. Sale prices are not recorded in public county records and are not required to be disclosed to any public body. The actual sale prices are recorded in the MLS, which is only accessible to licensed real estate professionals. This is why MLS-based pricing data is essential for accurate home pricing in Texas.

What MLS covers my area in Texas?

The four major Texas MLS boards are SABOR (San Antonio and surrounding areas), HAR (Houston and Harris County), ACTRIS/Unlock MLS (Austin and Central Texas), and NTREIS (Dallas-Fort Worth and North Texas). Your listing will appear on the MLS that covers your property's location. Waymark covers all four.

How is Waymark's pricing analysis different from a traditional CMA?

Waymark's AI, Aria, builds a pricing analysis using comparable sales data for your zip code. The difference is seller control: you can review every comp, remove ones that are not fair comparisons, and watch the recommended range update in real time. On the Manage plan, a licensed broker reviews the analysis before your listing goes live. Traditional CMAs are prepared by an agent and presented as a finished report. Both use comparable sales data. Waymark puts the seller in the driver's seat.

Price It Right the First Time

A Comparative Market Analysis is not a formality. It is the foundation of your entire selling strategy. In Texas, where actual sale prices are locked behind MLS access, a CMA built on real data is one of the most valuable tools you have.

Whether you are working with a traditional agent, using a flat fee MLS service, or listing through Waymark, do not skip this step. The homes that sell on time and at full value in 2026 are the homes that were priced right on day one.

Use our interactive comparison tool to see how Waymark's pricing analysis and transaction support compare to other listing options.

Waymark Real Estate | TREC License 639078 | Brokered by Marelli Properties

Related Articles

- How to Price Your Home Without an Agent in Texas

- How to Choose the Right Way to Sell Your Texas Home

- What Closing Costs Does a Seller Pay in Texas?

- Best Flat Fee MLS Companies in Texas (2026)

- What Is Fixed-Rate Selling?

Sources

- HousingWire, "What 10 years of data reveals about 2026 housing market signals," housingwire.com, April 2026

- HomeLight, "How Much Does a Comparative Market Analysis Cost?" homelight.com, March 2026

- Rocket Mortgage, "What is a CMA in real estate?" rocketmortgage.com, December 2025

- Chase, "Comparative Market Analysis Guide," chase.com, April 2026

- Luxury Presence, "CMA Real Estate Guide 2026," luxurypresence.com, April 2026

- Texas Realtors, "What Non-Disclosure Doesn't Mean for Reporting Prices to the MLS," texasrealestate.com

- SoldFast, "Non-Disclosure States 2026," soldfast.com, March 2026

- Absolute Properties HTX, "How to Get a CMA in Houston 2026," absolutepropertieshtx.com, April 2026

- Redfin, "Non-Disclosure States in Real Estate," redfin.com, November 2025

- NAR, "Listing Price Reduction: How to Navigate It," nar.realtor, August 2025